Branch or Digital – which drives customer experience more for retail banks?

Recent expansions of Nationwide and Metro Bank’s branch networks led alva to use our proprietary analytics to look at the impact that branches have on reputation compared to digital (defined as online and mobile) channels.

The analysis investigates:

- Which channel has the most impact on a bank’s customer experience?

- What is the customer sentiment trend towards the two channels?

- What are the implications of technology for future customer experience?

Which channel has the most impact on a bank’s reputation: branches or digital?

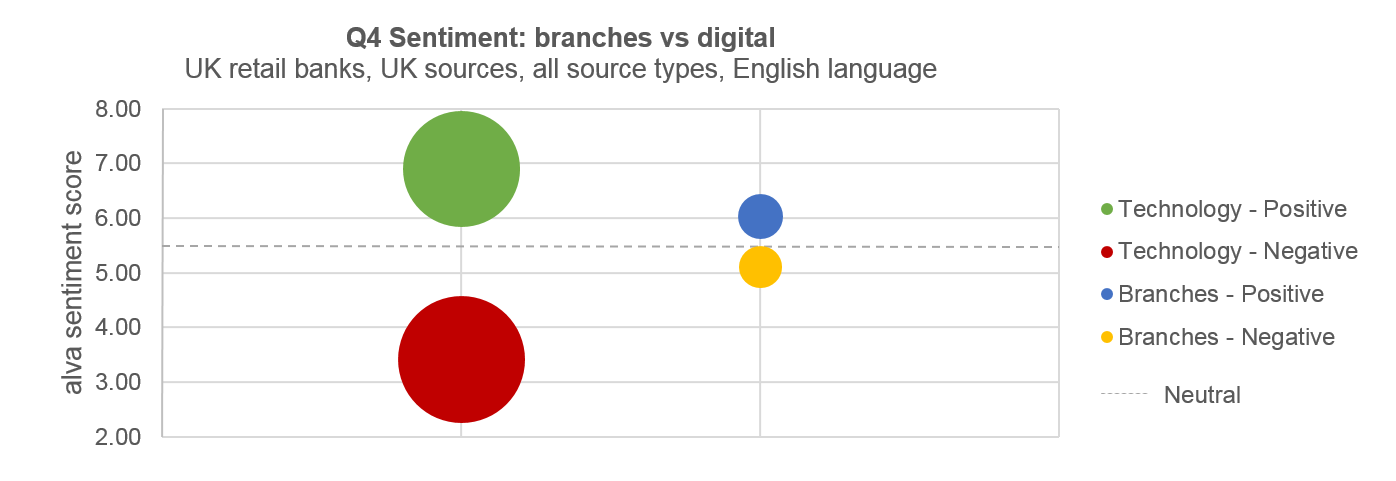

To answer this question, we analysed customer sentiment towards retail banks’ digital and branch channels. The graph below shows the sentiment score for each (y-axis), while the size of the bubble represents volume of content

Results

The positive sentiment score around digital channels exceeds the positive sentiment score for branches by a difference of +0.42 points out of 10.

Below the neutral line (indicated by a score of 5.50), the negative sentiment that surrounds digital channels is more critical than that of branches, with a difference -0.74 points.

Answer: Which banking channel has most impact: branches or digital?

Digital had a greater impact on sentiment than branches. The channel has both a larger positive and a bigger negative effect on the banking sector overall, a finding that remains consistent at monthly and weekly levels.

This data shows that getting the delivery of banking services right using digital channels has the greater leverage in improving a bank’s reputation. However, fail to get it right, and digital channels have the greater consequence.

What is the sentiment trend towards the two channels?

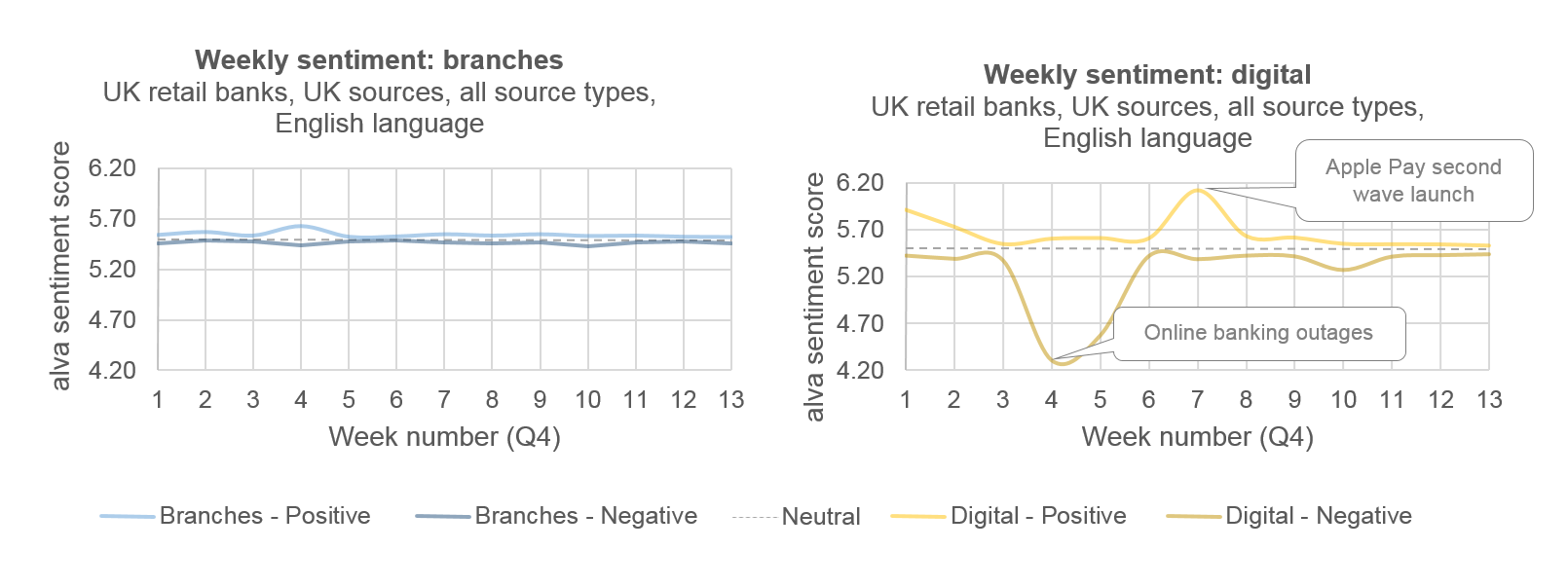

For this question, we analysed customer sentiment towards retail banks’ digital and branch channels day-by-day and week-by-week in Q4 2015 to gain insight into the differences between branch and digital channels. The graphs below show the sentiment score by channel (y-axis), for each of the 13 weeks of Q4 2015 (x-axis).

Result

The relative “flatness” of sentiment scores towards the branch channel contrasts with significant peaks and troughs in positive and particularly in negative sentiment scores for digital (online and mobile banking) channels. This is partly a reflection of exposure: digital volumes are over 30 times higher than branch volumes, posing greater volatility of sentiment expressed towards digital channels than branches.

The data also appears to show digital channels are more brittle; they are more vulnerable to “shocks”. These tend to have the overall effect of weighing down on the channel’s sentiment scores, with the negative shock deviating from neutral by almost -1.30 points, close to double the positive shock of +0.70 points. This may be due to the uniformly negative reaction to negative shocks such as an online outage, compared to the mixed reactions to positive shocks such as the “brilliant” or “late” launch of Apple Pay.

Answer: What is the sentiment trend towards the two channels?

There is greater volatility of sentiment through digital channels than the branch channel. Whilst an inherent bias may be expected in data collected from non-traditional sources such as social media, these sources form only part of the data captured and analysed by alva, which includes all publically available data and multiple stakeholder data.

Sentiment towards digital channels is also more unstable, and this volatility makes the channel more vulnerable to shocks.

Conclusion

- Digital channels are more impactful than branches on sentiment towards banks

- Short term shocks are a key influencer of overall sentiment and more prevalent in digital channels

- Online and mobile banking channel advancements will be a strategic lever for the UK banking sector going forward, with the power to boost or hinder banks’ reputations

Customer sentiment is most intense towards digital compared with branches, generating both a greater degree of positive sentiment (+0.42 points more than branches) and negative sentiment (-0.74 points lower than branches).

Furthermore, higher volumes for digital channels increase the volatility of sentiment, making short-term shocks a key influencer of overall sentiment. As a result, these “shocks” are a key risk to – and a potential opportunity for – shaping customer sentiment towards UK retail banks. If digital channels continue to have a greater influence on customer sentiment than branches, advancements in mobile and online technology such as bitcoin, biometric authentication and mobile payment services will need to become a strategic priority, potentially boosting and hindering the fortunes of the sector.

Footnote: The methodology – how do we calculate sentiment scores?

The alva algorithm calculates sentiment scores out of 10, where a score of 5.50 is considered neutral. The algorithm takes into account the volume, influence, prominence and relevance of real-time mentions from 80,000+ news sources, more than 3m blogs and forums, 100+ social networks. A score above 6.00 is considered strong, while a score below 5.00 is considered weak. “Digital” refers to mentions of online and mobile channels, including for customer service and everyday banking.

Be part of the

Stakeholder Intelligence community